Introducing FLIP 2.1: Fixed Supply, Revenue-Backed Staking

FLIP 2.1 ends token emissions, fixes supply, and redirects the protocol's daily FLIP purchases directly to stakers, delivering real, revenue-backed yield instead of inflation-funded rewards.

After months of internal discussion, community debate, and economic modelling, we've landed on a direction for FLIP 2.0 that we're confident in.

Here's the short version: emissions stop, supply becomes fixed, the protocol keeps buying FLIP every day, and instead of burning it, that FLIP goes directly to stakers.

The Background

Two schools of thought have dominated the FLIP 2.0 discussion.

One camp wanted protocol revenue paid out as USDC directly to stakers. The issue we found with this design was that it kills the protocol's structural bid. The ~$350k/month in FLIP market purchases disappears, and price support becomes fully dependent on organic demand.

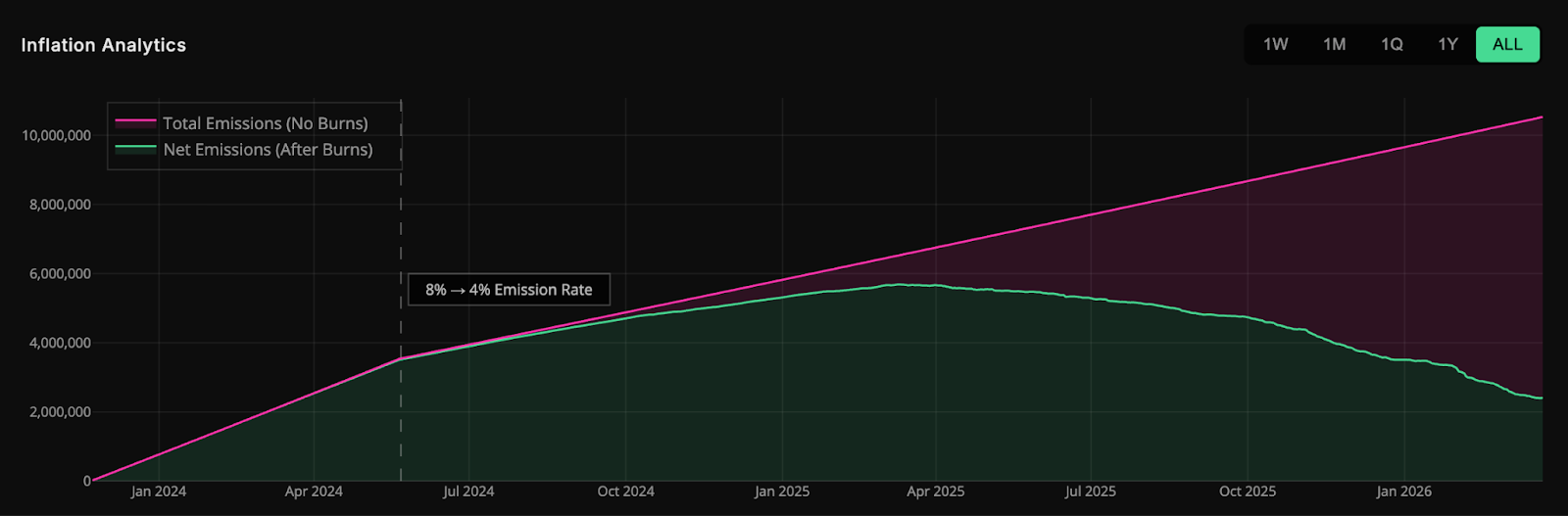

The other camp wanted to keep the current buy-and-burn model, maintaining the consistent buy pressure we are seeing, which would continue the meaningful supply reduction, recently in the range of 20–30k FLIP burned per day.

The issue with this approach was that staking yield is partially inflation-funded. Value accrual is indirect, and it benefits everyone passively, including those who aren't staking at all.

Both sides had valid points. Choosing one over the other meant accepting trade-offs that no one was happy with.

However, a middle-ground approach has surfaced that takes the best elements of both approaches, which we believe strengthens the FLIP token economic model and makes it a more attractive asset to hold.

What FLIP 2.1 Actually Does

FLIP 2.1 blends the two above approaches into one structure.

1. Emissions go to zero.

No new FLIP gets created. Supply is fixed from the moment of activation, and staking rewards are no longer funded by inflation. Every token distributed to stakers is backed by real protocol revenue. At the protocol level, this simply means setting emissions to zero, making it an easy change.

2. Buy-and-burn becomes buy-and-distribute.

The protocol's VTWAP buying mechanism stays exactly the same. The only thing that changes is what happens to the FLIP after it's purchased. Instead of being burned, it's distributed to validators and delegators.

The buy pressure remains intact. The protocol continues to act as a consistent daily buyer. The difference is that active participants now receive the FLIP directly, rather than benefiting indirectly through supply reduction.

Why This Is Stronger

Under the current model, staking yield is a combination of inflation rewards and the indirect benefit of burn-driven supply reduction. Under FLIP 2.1, yield is direct, revenue-funded, and automatically compounding.

Instead of inflating supply and burning it back down, we fix supply and redirect purchased FLIP to the people actually securing the network.

Here's how it works:

- Protocol earns fees.

- Fees buy FLIP off the market.

- That FLIP goes to stakers.

This will substantially boost yields for stakers and improve the value proposition of holding and actively staking FLIP.

The Numbers

Let's talk about what this actually looks like.

Right now, staking FLIP earns roughly 18.21% APY. That's a combination of inflation-funded emissions and the indirect benefit of burns. Not bad, but a chunk of that yield is dilutive.

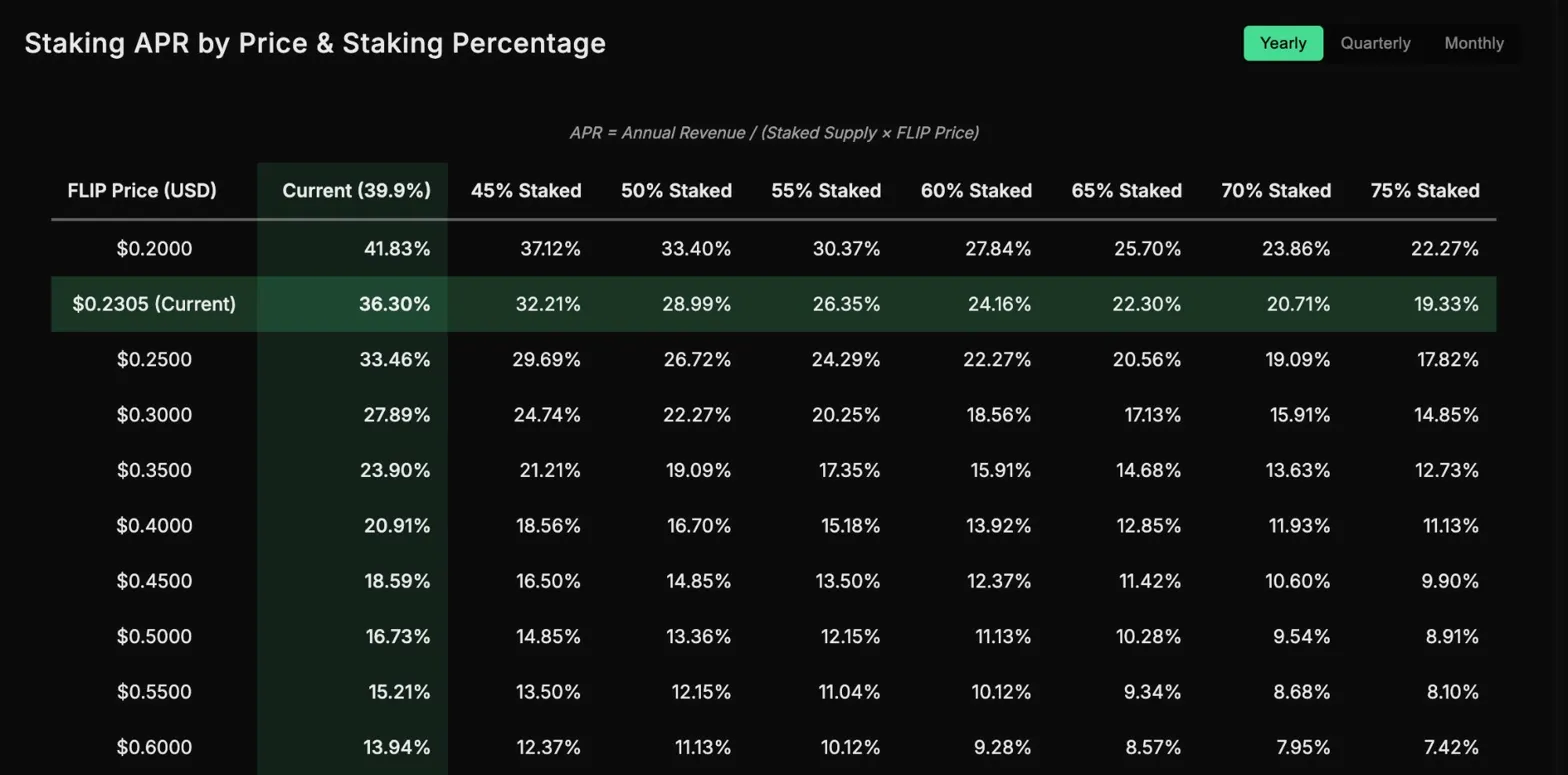

Under FLIP 2.1, with current revenue levels and the current staking ratio of ~40%, the projected staking APR jumps to 36.30% at today's FLIP price of $0.2305. That's real, revenue-backed yield. No inflation involved.

The table above shows how yields shift across different FLIP price points and staking percentages. Even in less favorable conditions, the numbers hold up well. At $0.50 FLIP with 50% of supply staked, you're still looking at 13.36% APR, funded entirely by protocol revenue. At current levels, with 45% staked, it's over 32%.

These yields aren't hypothetical. They're based on actual current protocol revenue. As volume grows, so do the fees, and so does the yield.

The key point: FLIP 2.1 doesn't just maintain staking returns; it significantly improves them while removing the inflationary component entirely. That makes FLIP a fundamentally more attractive asset to hold and stake.

What About Sell Pressure?

This is the most common concern, so let's address it directly.

Under the burn model, emissions continuously add supply. The burn offsets it, but it's a two-sided equation. FLIP comes in through emissions and goes out through burns.

Under FLIP 2.1, emissions are gone. No new supply enters circulation. The VTWAP buy continues removing supply from the market, and rewards are locked into stake. Accessing them requires active unbonding. We have seen through over 2 years of live network data that stakers typically do not sell their rewards. Stakers tend to be long-term committed to the project, and we therefore expect the velocity of staking rewards to remain low, meaning the bulk of the fee-driven protocol buying should remain in the system for extended periods of time.

Of course, operators still need to cover costs, but there is no structural difference between the current model and this 2.1 approach in that regard.

Validator Economics

Right now, validators get a baseline yield from emissions no matter what. Under FLIP 2.1, that yield comes from revenue. Validators do well when the protocol does well, which is a way to further value align the protocol's participants.

At current revenue levels, the yield from redirected FLIP purchases exceeds what emissions alone provide.

The risk scenario is a prolonged, severe drop in volume. If revenue contracts significantly, validator rewards contract too. But realistically, that scenario points to bigger protocol-level issues, not a token model problem. Even under a 50–70% revenue reduction, rewards decline but don't disappear.

If conditions ever get to a point where validator security is genuinely at risk, emissions could be reintroduced to cover shortfalls in minimum required revenues for operators, though we consider this an extreme and unlikely scenario.

The Rollout

Phase 1 - Communication (now): This post. FAQ to follow. We want complete clarity on what changes, what doesn't, and why.

Phase 2 - Development: The required changes in the protocol require modifications to the logic to allow for distribution of fee-derived FLIP purchases to validators and their delegators, which needs to be produced by the protocol team.

Phase 3 - Activation: After these upgrades have been included in a release and the frontends updated to account for this new economic model, the new method can be seamlessly switched on at any time. This includes setting emissions to zero, disabling the burn mechanism, activating the mechanism to redirect the purchased FLIP to the staking distribution module, and enabling auto-compounding.

The timeline for these steps will depend on the availability of protocol development resources and requisite product updates, though being relatively small changes, they could be concluded within a couple of months.

As a part of this upgrade process, improvements in the staking flow and overall product navigation should make it easier to display attractive yields to prospective stakers.

As a final point, these changes are readily reversible should the model prove to be less effective than anticipated, with the underlying code that runs the current buy-and-burn and emissions model remaining in place for now.

The Bottom Line

FLIP 2.1 moves the token from an inflation-assisted model to a fully revenue-backed system.

Fixed supply. Ongoing protocol buy pressure and revenue-funded yield.

The economic loop gets simpler, the incentive alignment gets stronger, and the value proposition for stakers gets clearer. As a reversible model change, we believe that experimenting with this solid proposal is a worthwhile endeavor that can be readily implemented with low risk.

Resources

- Swap Now - Start swapping native assets

- Lend BTC - Borrow against native Bitcoin

- Blog - Product updates and announcements

- Chainflip Scan - Track swaps and network activity

- Website - Explore Chainflip

Other Chainflip Products:

- Boost - Earn fees by providing single-sided liquidity with no IL risk

- Stablecoin Strategies - Deposit stablecoins and earn optimized yields

- Provide Liquidity - Supply assets to Chainflip's liquidity pools

- Stake FLIP - Delegate FLIP and earn staking rewards

Find us: